Tax Harvesting – Reduce your LTCG taxes for higher returns

In 2018, a 10% long-term capital gains (LTCG) tax was introduced when none existed before. The budget for 2024 further increased the LTCG tax rate to 12.5% for all classes of assets. This LTCG tax, however comes with a tax break.

The first Rs. 1.25 Lakhs of LTCG is exempt from the 12.5% LTCG tax.

Tax Harvesting is a technique that utilises the Rs. 1.25 Lakh annual LTCG exemption by selling and buying back your investment such that you “realise” gains and not pay taxes on the exempt Rs 1.25 Lakh of LTCG.

At a 12.5% LTCG tax rate, you could save up to Rs 15,625 in LTCG taxes every year by doing this diligently.

Ben Franklin famously said, “Nothing is certain except for death and taxes.” and Margaret Mitchell exclaimed, “Death, taxes and childbirth! There’s never any convenient time for any of them.”

Yes, no one likes paying taxes!

We, however, encourage every citizen to pay their rightful taxes for nation-building. That said it is also our responsibility to our financial future and to our children, to take advantage of tax breaks written in the tax code.

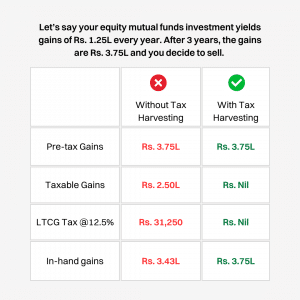

Let’s see a simple example of how LTCG Tax Harvesting works.

By harvesting Rs 1.25 Lakhs of LTCG every year, you reduced your LTCG Tax burden from Rs 31.2k to NIL.

This is the power of LTCG Tax Harvesting and we are bringing it to you.

How Tax Harvesting works?

It’s simple. We take over once you unlock the Tax Harvesting feature on Kuvera.

We monitor your portfolio and recommend a transaction when applicable. We use sophisticated modelling to decide when is the right time to harvest taxes. Then we recommend the transactions you need to execute to harvest LTCG.

As mentioned above, there are two opposing forces –

1. If I wait and the markets go up, I can harvest more taxes (something like 2017).

2. If I wait and the markets go down, I would have lost the opportunity to harvest the gains I had (something like 2018). And since tax harvesting is tied to the calendar year, once that opportunity goes, it won’t come back.

We run an optimization that solves for the above to ensure that you can harvest the optimal level of taxes as soon as possible.

The power of LTCG tax saving is now on your fingertips. Try it now.

Frequently Asked Questions

(Q) Why can’t I wait till Feb – Mar and harvest then?

(A) We would advise harvesting taxes as early in the Financial Year as possible.

There are two opposing forces –

1. If I wait and the markets go up, I can harvest more taxes (something like 2017).

2. If I wait and the markets go down, I would have lost the opportunity to harvest the gains I had (something like 2018). And since tax harvesting is tied to the calendar year, once that opportunity goes, it won’t come back.

We run an optimization that solves for the above to ensure that you can harvest the optimal level of taxes as soon as possible. Waiting after the optimal condition is met only increases the likelihood that the LTCG may not be there in the future to harvest.

(Q) I have subscribed to Tax Harvesting and I have a family account. Will my subscription cover all accounts?

(A) Tax Harvesting is enabled based on the taxpayer PAN. Say for example a husband and wife have 4 accounts –

- Wife’s Single

- Husband Single

- Wife + Husband Joint

- Husband + Wife Joint

If the Wife then enables Tax Harvesting in her account it will also enable it for Wife + Huband Joint account as for tax filing purposes LTCG in both the Wife and Wife + Husband account will be attributed to Wife’s tax returns. So, you will have to enable Tax Harvesting individually for every taxpayer in your family. In our example, it would mean to enable Tax Harvesting for Wife and Husband separately.

(Q) I have a few funds with considerable profits, but Tax Harvesting never recommends harvesting tax in them?

(A) Even if you have funds with considerable Long Term Capital Gains, there could be reasons why we don’t show them for Tax Harvesting. Chief among those reasons are –

- The fund is still under lockin. This is particularly true for ELSS and other speciality schemes.

- The fund house does not allow lumpsum purchase in the fund. For efficient tax harvesting, you have to be able to buy back the scheme at the same NAV.

(Q) If I sell now to harvest LTCG, will I lose out on future profits from that investment?

(A) Not at all. As part of Tax Harvesting, we will advise you to sell the units and buy it back with no NAV impact. So you will still get the benefits of all future profits if that investment continues to go up.

Start investing through a platform that brings goal planning and investing to your fingertips. Visit kuvera.in to discover Direct Plans and start investing today.

#MutualFundSahiHai, #KuveraSabseSahiHai!