a sip is a method of investing in mutual funds. a fixed amount gets deducted regularly. monthly. quarterly. weekly. the money buys units of a fund at the prevailing nav .

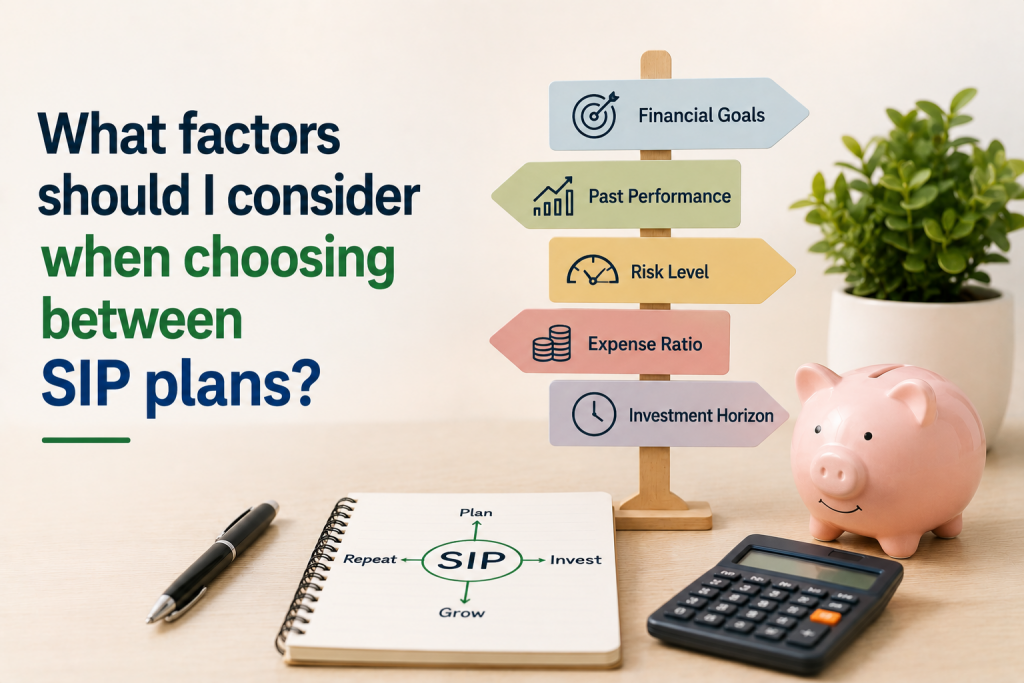

the choice of sip plan depends on a few things. financial goals. risk tolerance. investment horizon. these three factors decide which fund category works .

financial goals. the starting point.

every investment needs a purpose. without one, selecting a fund becomes random.

short-term goals. 1 to 3 years. emergency fund or a vacation . debt funds or liquid funds work here. low risk. stable returns .

medium-term goals. 3 to 5 years. saving for a car or a down payment . hybrid funds can work. they balance equity and debt .

long-term goals. 5 years or more. retirement or child’s education . equity funds are more suitable. higher growth potential over longer periods .

the goal determines the fund category. not the other way around.

risk tolerance. how much volatility can be handled.

equity funds offer higher returns. they also come with higher risk . debt funds are safer. but returns are lower .

someone who cannot tolerate sharp swings should avoid mid-cap and small-cap funds. large-cap funds are relatively stable . a moderate risk profile may suit hybrid funds .

the choice should match the investor’s comfort level. not the fund’s past performance .

investment horizon. time matters.

the period for which money can stay invested is critical. short-term goals need safer options . long-term goals can take more risk .

equity sips have historically delivered better returns over 10-year periods . but they need time to smooth out volatility . the longer the horizon, the more compounding works.

fund performance and consistency

past performance does not guarantee future returns . but it offers useful data.

check returns over 3, 5, and 10 years . compare with the fund’s benchmark. look at consistency across different market cycles.

a fund that performs well in both bull and bear markets is usually better managed.

expense ratio. the cost matters.

this is the annual fee charged by the fund. deducted from returns. higher expense ratio means lower net returns over time .

direct plans have lower expense ratios than regular plans. no distributor commission. more of the money stays invested.

for long-term sips, even a 0.5% difference in expense ratio can affect the final corpus.

fund manager and investment strategy

the fund manager’s track record matters . check their experience. look at the funds they manage. see how those funds performed across market cycles

also check the fund’s investment strategy. what sectors it focuses on. how diversified the portfolio is . a strategy that matches the investor’s preferences is important.

sip amount. staying within budget.

the sip amount should not strain monthly cash flow. start small. increase gradually as income grows . a step-up sip can automate this increase .

using a sip calculator helps. it shows the monthly investment needed to reach a specific goal . this keeps expectations realistic.

types of sips. matching the need.

| sip type | what it does | best for |

|---|---|---|

| regular sip | fixed amount every month | beginners with stable income |

| top-up sip | amount increases at set intervals | salaried people with regular hikes |

| flexible sip | amount can be increased or paused | those with fluctuating income |

| perpetual sip | no fixed end date | long-term goals like retirement |

regular sip is the most common starting point. top-up sip helps keep pace with income growth. flexible sip suits freelancers or business owners.

common mistakes to avoid

choosing funds based only on past returns. this is the most common error. returns change. consistency matters more .

stopping sips during market corrections. this defeats the purpose. lower prices mean more units for the same amount . staying invested through volatility is what makes sip work .

ignoring expense ratio. a higher fee eats returns over time. direct plans are cheaper .

not reviewing investments periodically. goals and market conditions change. checking once or twice a year keeps things on track .

frequently asked questions

1. which sip type is best for a beginner

regular sip is the simplest. fixed amount. fixed interval. stable income works best .

2. how much should be invested in a sip

the amount should fit the monthly budget. start with what is comfortable. increase gradually. use a sip calculator to see if the amount meets the goal .

3. is a mutual fund sip safe

sips reduce timing risk. they do not remove market risk. equity sips can fall in value. debt sips are safer but offer lower returns .

4. how does a top-up sip work

the sip amount increases automatically at set intervals. fixed amount or percentage. suits salaried people with regular income growth .

5. should sips be stopped when markets fall

no. continuing during a fall buys more units at lower prices. this is how rupee-cost averaging works .