First, for those who are new to Kuvera, a quick recap.

We have recommended a portfolio since Jan 2017. We updated our recommendation in Oct 2018. You can read about that here: Performance & Recommended Portfolio Update

We started out in Jan 2017, with this equity portfolio –

| Jan 2017 – Oct 2018 | Portfolio Weight |

| ICICI Prudential Nifty Next 50 | 45.7% |

| Motilal Oswal Focused 25 | 28.5% |

| IDFC Nifty | 12.9% |

| ICICI Prudential US Bluechip | 12.9% |

We updated it in Oct 2018, to our current equity portfolio recommendation –

| Oct 2018 – Till Now | Portfolio Weight |

| UTI Nifty Next 50 | 45.7% |

| Motilal Oswal Focused 25 | 28.5% |

| DSP Equal Nifty 50 | 12.9% |

| ICICI Prudential US Bluechip | 12.9% |

We recorded the rationale for portfolio recommendation changes here: Performance & Recommended Portfolio Update

Our portfolio has ~13% international exposure through ICICI Prudential US Bluechip fund. Has focused factor exposure through ~29% holding in Motilal Oswal Focused 25 fund. You will also note that with the exception of Motilal Oswal Focused 25, the remaining three funds have zero stock overlap.

Second, how do I see Kuvera’s recommended portfolio?

You can view our recommended portfolio and invest in it when you do goal planning on our platform. You can also just mimick the portfolio weights above. The difference is that when we know your goals and your investment horizon (5 yr, 10 yr etc) we can also advise you on how much of your portfolio should be in our recommended equity portfolio and how much should be in our debt portfolio. So, goal planning will not only show you our recommended portfolio but also asset allocation.

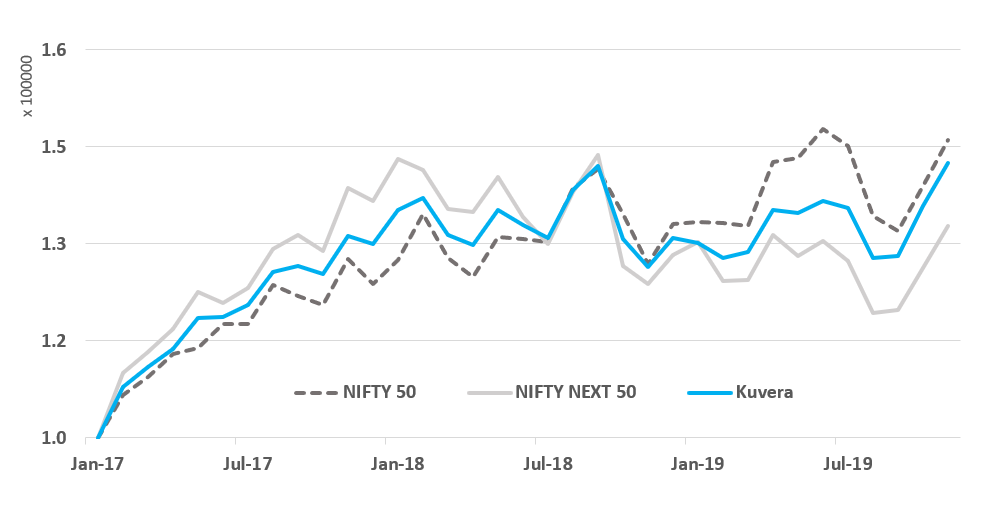

That out of the way, let’s look at the performance and risk review of our portfolio vs Nifty 50 and Nifty Next 50.

Performance overview – all time period.

| Jan ’17 – Oct ’19 | Nifty 50 | Nifty Next 50 | Kuvera |

| Annual Return | 14.3% | 10.5% | 13.3% |

| Std Dev | 13.5% | 15.7% | 12.2% |

| Drawdown | -10.7% | -17.1% | -11.0% |

| Max Monthly | 7.4% | 10.1% | 7.9% |

| Min Monthly | -7.5% | -12.0% | -8.0% |

| Return / Risk | 1.06 | 0.67 | 1.09 |

And the chart:

Some quick observations:

1/ Our rationale of the four selected funds was based on low historic covariance and low fund overlap. In the case of index funds, we used index returns to have long-run data available. Nifty Next 50 is the base of our recommendation with 46% of our equity portfolio recommended to this index. Our diversification through Nifty index, one international fund and one focused fund significantly improve on the return and risk of Nifty Next 50. Nifty Next 50 reward to risk ratio (Returns / Std Deviation) has been 0.67 in this time period while the Kuvera portfolio has a reward to risk ratio of 1.09. Since Jan 2017, while Nifty Next 50 has returned 10.5% annualized our diversified portfolio has returned 13.3% annualised. Similarly, while the volatility of Nifty Next 50 has been 15.7% our recommended portfolio has a volatility of 12.2%.

2/ That Nifty 50 and our returns are close is a co-incidence. Nifty 50 has returned a higher 14.3% during this time period at a marginally lower reward to risk ratio (1.06 vs 1.09). That our returns are close to Nifty 50 is a pure coincidence. We expect this to diverge in the future.

Performance overview – calendar year performance.

| Return | Nifty 50 | Nifty Next 50 | Kuvera |

| 2017 | 27.6% | 43.2% | 35.2% |

| 2018 | 4.5% | -9.0% | -3.7% |

| 2019 YTD | 9.5% | 1.9% | 9.5% |

| Volatility | Nifty 50 | Nifty Next 50 | Kuvera |

| 2017 | 11.1% | 13.1% | 9.3% |

| 2018 | 15.4% | 18.2% | 14.3% |

| 2019 YTD | 14.3% | 14.0% | 11.9% |

| Reward / Risk | Nifty 50 | Nifty Next 50 | Kuvera |

| 2017 | 2.5 | 3.3 | 3.8 |

| 2018 | 0.3 | -0.5 | -0.3 |

| 2019 YTD | 0.7 | 0.1 | 0.8 |

What next?

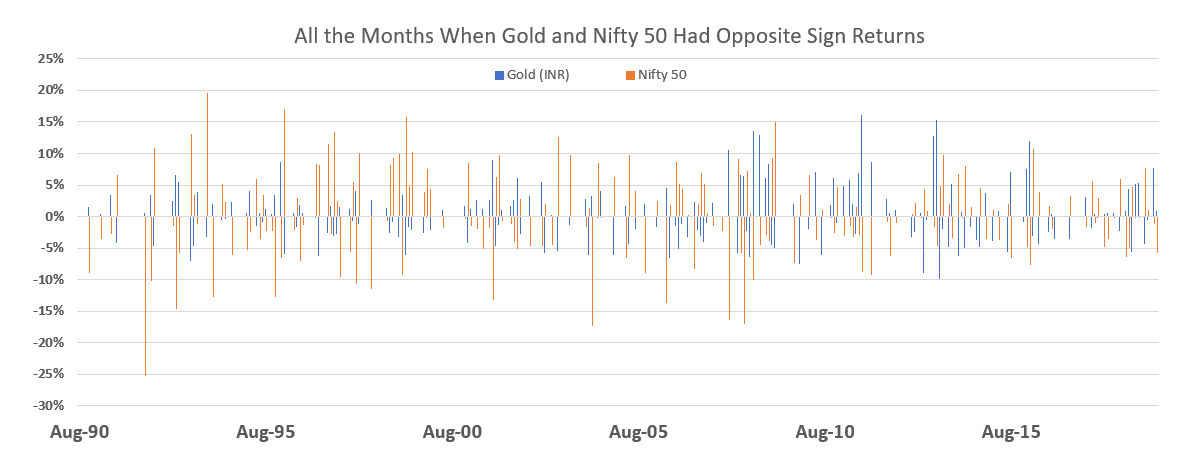

We have written on how gold can be a good downside hedge to equity exposure – even better than credit and bonds. In the past 29 years of data, the correlation of monthly gold returns and monthly Nifty50 returns is just 0.3%!

Of the 348 monthly returns in our sample, there are 178 instances where the returns on gold and returns on Nifty 50 have opposite signs. That is if gold posted positive returns, Nifty 50 posted negative returns and vice versa. This is exactly what diversification is about – two assets, each with positive expected returns but no correlation in returns.

Essentially, what gold loses in return expectation it more than makes up for in correlation and thus diversification benefits. Gold, you see, is a team player. And at times when Nifty 50 is not performing due to crash fears, wars, natural hazards or disasters, gold does well.

It helps you tide over the bad times much better. Or you could say, when the going gets tough, gold gets going.

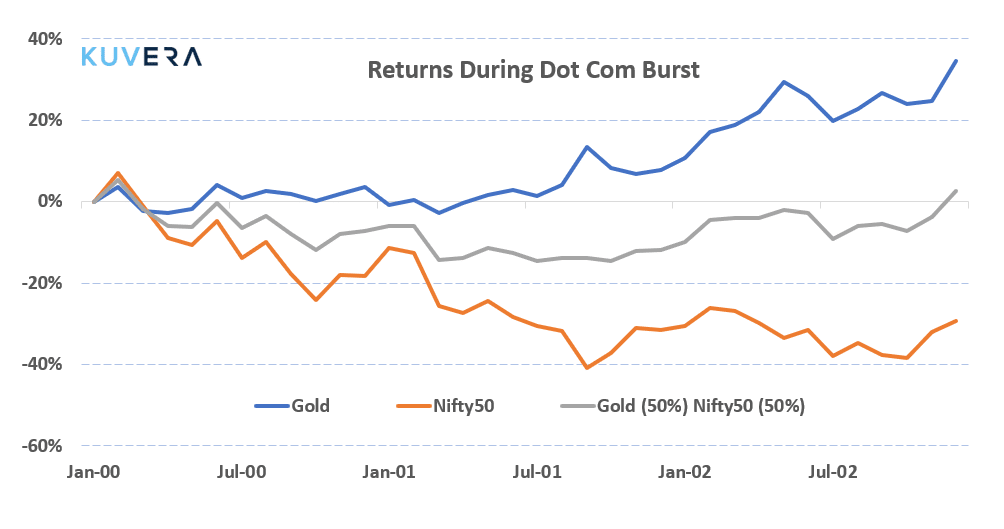

The dot com burst of 2000 – 2002: Between 2000 to 2002 Nifty50 proceeded to fall 40%. As a flight to safety and crash hedge, Gold had outsized gains of ~30% during the same time period.

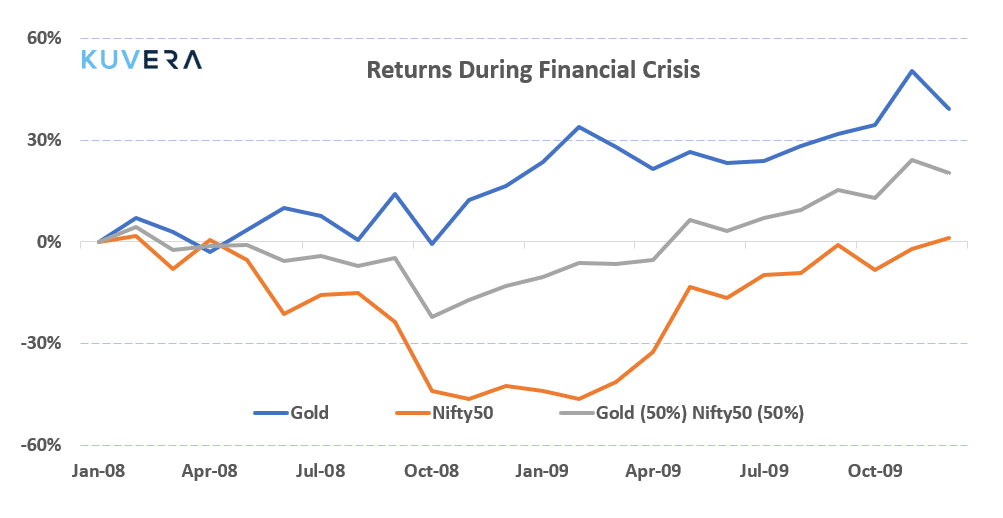

The Global Financial Crisis of 2008: Nifty50 saw a monthly drawdown of ~50% during that time. Gold again shone as the crisis hedge and rallied ~30% to protect from some of the impacts of the stock market meltdown.

We also note that digital gold is probably the best way to get exposure to the yellow metal, far better than gold ETF and Mutual Funds.

Frequently Asked Questions

1/ How often should I rebalance?

You can allow a 5% deviation to model allocation before thinking of rebalancing to original portfolio weights. Deviation based rebalancing is far superior to time-based rebalancing (every 3 months, or 6 months etc).

2/ When will you add small-cap exposure?

We are still tracking small-cap and mid-cap space with interest. This was our position in Oct 2018 as well when we did our last portfolio update. We are still not convinced this space offers value and we are comfortable to the possibility that we might miss the bus on a small-cap bull run. There is no FOMO. We will keep you informed as and when our opinions change.

3/International markets are doing well, should we increase our US exposure?

No. In 2017, the Indian market did very well and we were questioned on our US exposure. Then 2018 and 2019 happened. Diversification is not the same as chasing returns. If you do not have international exposure then it helps to add it to your portfolio. If you already do, then don’t increase it based on recent past returns. Chasing returns will only lead to the behaviour gap and lower future returns.

*** We will keep adding FAQ based on what we get asked the most 🙂

Interested in how we think about the markets?

Read more: Zen And The Art Of Investing

Watch/hear on YoutTube:

Start investing through a platform that brings goal planning and investing to your fingertips. Visit kuvera.in to discover Direct Plans and start investing today.

#MutualFundSahiHai, #KuveraSabseSahiHai!