Stronger for Longer. That’s @abslmf’s Annual Outlook for CY2024.

Here’s a quick look at the headlines.

Just in case you missed it, check out @Kuvera_In’s insights from investors – India Rising | 2023 Review and 2024 Outlook.

Download: https://kuvera.in/IndiaRising_2024Outlook

Global economic growth exceeded expectations. In India, it was investments, not consumption, that primarily fueled this progress.

A look at the distribution of S&P BSE Sensex returns over the years

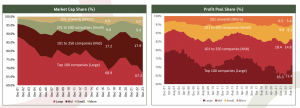

The breadth of Indian equity markets increased even as large-caps increased their share of the total profit pool.

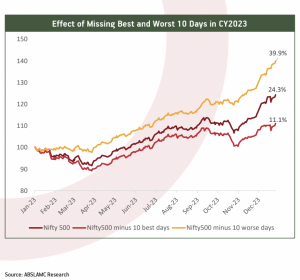

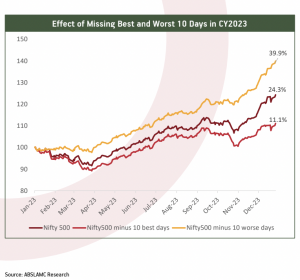

Amidst the market rally in a low-volatile environment, just remaining invested in the market gave ~25% return.

Remember, time in the market is more important than timing the market.

——–

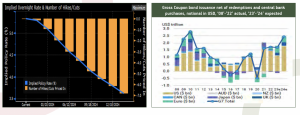

China PPI has generally led US inflation and is signaling further slowdown, the report says.

Money supply is normalizing; major Central Banks’ balance sheets contracting.

Wage growth remains high but is moderating due to a robust rebound in labor supply.

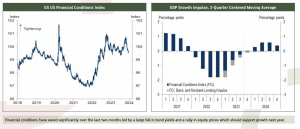

Improved US financial conditions are expected to positively impact growth in the upcoming year.

Consumption growth has normalised and is anticipated to further decelerate in the upcoming year.

Expectations of six interest rate cuts in the upcoming year pose risks to bond prices, exacerbated by substantial issuances.

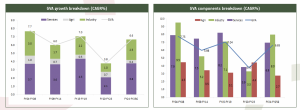

India’s growth is expected to remain strong at 7% YoY for FY24 and 6.5% YoY for FY25E, driven by investments, government capex, housing sector revival, & improved consumption from previous lows.

The growth composition of FY24-25E is expected to be like FY04-08 period with industry from the supply side and GFCF from the demand side being the key driver of growth.

‘@abslmf expects steady fiscal consolidation by the government on the back of strong tax collections & reduction in revenue expenditure and fiscal deficit declining to 5.4% in FY25E.

Uptick in the housing cycle is a big positive for the economy. The decline in gross fixed capital formation since the early 2010s was led by the housing sector & we are witnessing long-term revival for the same.

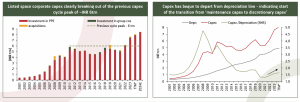

Private corporate investment is rebounding, seen in rising orders for capital goods & ongoing project implementation, with high capacity utilization signaling an imminent uptick in capex.

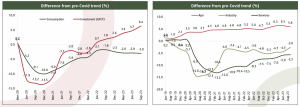

The growth trend since the onset of Covid shows stark divergence between consumption & investment, with investment growth significantly moving above pre-Covid, aided by strong government push, but consumption remains lagging.

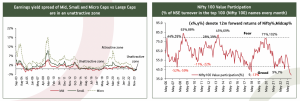

Expecting lower inflation, it’s forecasted to ease from 5.45% in FY24E to 4.6% in FY25, driven by a food-price surge in FY24 that’s expected to subside, aligning with lower core inflation at around 4%. This sets the stage for policy normalization.

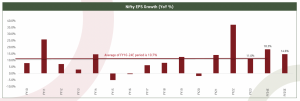

Nifty earnings growth is expected to be ~15% in FY25E driven by sectors such as banking, auto, industrials, infrastructure, cement, and real estate.

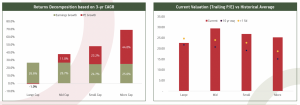

Amidst market consolidation and earnings revisions, large-cap valuations remain reasonable.

While large cap returns have been driven largely by earnings growth, a large part of the returns for midcap, smallcap & microcap segments have been driven by a re-rating in the valuation multiple.

While there is a structural positive outlook for mid & small caps in the medium to long term, short-term volatility may arise in this segment due to valuation catch-up & relative valuation comfort in large caps.

Over a 3-year period, Value has outperformed Growth, but this trend may shift as interest rates are expected to decrease in 2024.

Value has surpassed Quality over a 3-yr period, but this may change as investor sentiment improves & they shift away from Value stocks.

Private capex has started picking up and the capex cycle is turning broad-based

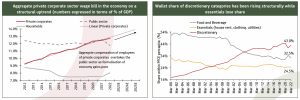

Economic formalization and wage growth boost: A surge in disposable incomes has driven higher discretionary consumption.

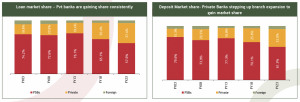

Although Private Banks have consistently gained share over PSU Banks, easy wins may be over and incremental profits will be linked to economic growth.

@abslmf‘s Asset Class Expected Return for CY24

Equity ? 10-15%

Fixed Income ? 8 – 9%

Gold ? 5-10%

Prefer largecaps in equities, aiming for median equity allocation. For CY24, expect solid fixed income returns. Diversify and tactically boost fixed income.

Those were the highlights of @abslmf’s 2024 Outlook.

Interested in how we think about the markets?

Read more: Zen And The Art Of Investing

Watch here: Investing through various economic and market cycles

Start investing through a platform that brings goal planning and investing to your fingertips. Visit kuvera.in to discover Direct Plans and Fixed Deposits and start investing today.